Tax tips for landlords

Owning a rental property portfolio that provides an income is much like owning a business, and as such there are tax implications and dues that need to be paid to the South Africa Revenue Service.

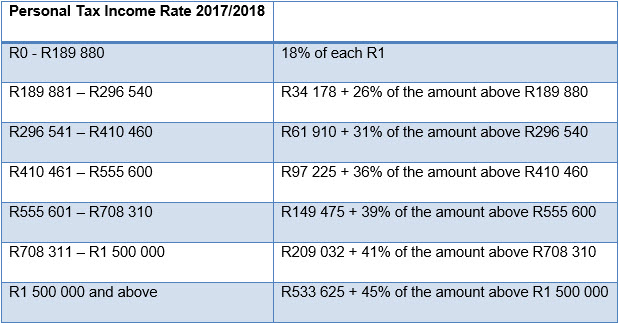

According to Adrian Goslett, Regional Director and CEO of RE/MAX of Southern Africa, landlords are required to declare the total amount of rental income received as gross income and they will be taxed at the marginal Income Tax Rate, applying to the owner of the home. The below table is a guideline of the personal tax rates that are currently applicable in South Africa:

Goslett notes that while landlords are required to declare the total income acquired through letting out their property, there are certain deductions that can be made, such as a non-capital expense. A landlord is obliged to incur expenses during the period that the property is let out. “Deducting the non-capital expenses from the landlord’s tax return will reduce the taxable income and possibly put the landlord in a lower tax bracket, which will be of benefit to them,” says Goslett.

He notes that examples of non-capital expenses include the following:

- Rental agent’s commission or fees for securing a tenant

- Advertising costs of marketing the property

- Insurance fees, levies, municipal rates, water and electricity

- Interest paid on the home loan if applicable

- Cleaning costs, garden services and security

- If the property is furnished, the depreciation of the furniture’s value can be deducted

- Legal fees incurred from disputes with tenants – this includes the eviction of tenants

- Repairs and maintenance costs – this does not include improvements to the property

Goslett says that expenses that are regarded to be of a capital nature cannot be deducted. These would include any expenses incurred while renovating or adding on to the property. “If the tenant has moved out of the property and the landlord decides to make repairs to the home to sell it, these expenses cannot be deducted as they did not happen while the tenant occupied the property,” he adds.

If the total of the deductions exceeds the rental income received by the landlord and they wish to declare a net rental loss, the Income Tax Act contains a ring-fencing provision that may come into play depending on the circumstances. If the provision does apply, the landlord will not be able to offset their rental losses against income received from other sources.

Goslett warns that evading paying tax on rental income will see the landlord in deep financial water. “Rental agents are obligated to provide SARS with a record of the rental income received and paid over to the landlord. As a result, it is very easy for SARS to find any discrepancies in the landlord’s tax return. If found out evading tax after notification of an audit, the landlord could be facing a hefty penalty or worse - imprisonment,” he explains.

In conclusion, Goslett says that all rental income should be included in the landlord’s taxable income. However, reducing it by the relevant expenditure will assist the landlord to reduce the amount of money that leaves their back pocket.

{kind=link}

Send to a Friend